|

The guest posts continue on the savings and retirement theme. But this time with a twist. Tuck in, this is a longer read.

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.” ― Henry Ford. We need to start talking about inflation, pensions, and Bitcoin. Inflation erodes the capital value of savings and diminishes the burden of debt obligations. It also inflates the nominal value of assets held by lenders as collateral, making them appear to be worth more. So inflation simultaneously makes debts less significant, and balance sheets appear to be healthier. Governments are the largest borrowers in the world. They are therefore the largest beneficiaries of inflation, as the real value of their debt is diminished at the expense of the purchasing power of their currency. Tax revenues go up and government debt becomes a smaller percentage of government revenue raised from taxes. This is an old playbook, and it's the reason why government issued fiat currencies almost always eventually collapse. There is a built in incentive for governments to dilute their currency to reduce their cost of borrowing, and one area that people need to start thinking about how this applies to is pensions. Government debt is growing from both deficit spending and interest- it's just a matter of at what rate, while it may ebb and flow inflation is unlikely to go away. So understanding this, means accepting that the money supply is very likely to continue to expand and dilute over time. It also means if you are counting on a pension payout, be it Defined Benefit, or Defined Contribution Benefit, IPP, PPP, or RRSP plan - the real world value of those benefits you receive at time of collection is likely to be inflated away. Understanding this fundamental problem, we have to start examining how prolonged currency inflation forces us consider new ideas for growing and preserving the value of our hard earned money. It is why we have seen large pensions get more creative with their investments, and more aggressive in their asset mixes. It is also why Bitcoin is unique as an asset that can and should be incorporated into pensions and retirement planning. 21,000,000 /♾️ The permanently fixed supply of Bitcoin, capped at 21 million- might not strike universally today as a gold standard characteristic of an asset to hinge part of your planned retirement on. Consider the above problem that government money, essentially must continually expand - to meet the needs of new projects, and to degrade the value of the amount already borrowed. There will only ever be 21 million Bitcoin. That means if we are considering the title chart comparing the supply of Bitcoin to the balance sheet of the US Federal Reserve, that graph can essentially diverge infinitely. Bitcoin exists as a verifiably hard asset, in a financial universe built on planned infinite expansion. Now consider that Bitcoin is an asset that anyone in the world with a cellphone can buy, and that every government in the world has a debt problem. As the supply curves diverge further and further, Bitcoin will become an infinitely improving caliber of asset to be held for the preservation of value. Volatility - Horizon is a crucial component of investing for retirement, and Bitcoin critics will point to its short term volatility as a reason why it can not be counted on as a vehicle for retirement planning. Bitcoin is volatile today and year to date it is down almost 40% in price. If you are planning to retire in the next 6 months, you might not want to go all in. I am not suggesting Bitcoin is the silver bullet, merely that pension committees and self-directed plan members alike need to start thinking about having an allocation to Bitcoin because of the inherent need governments have to print money to keep the current system going. The question of long-term concern about volatility can be looked at a few ways. To keep the length of this manageable I am just going to examine one. Bitcoin today is roughly a $600,000,000 USD asset. The global market cap of gold is somewhere between 12-15 trillion USD. Stocks, real estate, and cash are in the hundreds of trillions. Your long-term view of the volatility concern in my opinion should be this- How big do you think Bitcoin as an asset can get? I say this for a few reasons but most importantly it stands to reason that the larger it becomes, the harder the needle becomes to move violently down. When we arrive at a point where 12 trillion USD have found their way to Bitcoin, it stands to reason that producing a 3 trillion USD outflow needed to crash the price would take a degree of collective panic orders of magnitude higher than the mere billions of dollars required to do it today. The bigger assets get, the less volatile they tend to be. Keep in mind, the total global money supply has to continually expand, at varying speeds. Even if Bitcoin for some reason stops gaining new users today - the asset would likely still grow over time even if it only continued to capture on a percentage basis the same amount of available money that it is today, but it is growing in new users. The Bitcoin network is adding users faster than the internet did in the late 90s. So think about that and ask yourself - Bitcoin is the fastest asset to reach 1 trillion USD ever. Is it more likely that over time Bitcoin will cease to exist or continue to grow, as a superior deflationary asset in an inherently inflationary world? Returns - There are two ways to look at this in my opinion. One is, how can we expect Bitcoin to appreciate in price compared to other investments over time? The other is to invert that question and consider how will other assets compete with Bitcoins ability to endlessly appreciate in price? As the money supply continues to expand over time the value gap between the value of government currency with an unlimited supply and Bitcoin with a permanently fixed supply will only become more dramatic. The other assets that would typically comprise a pension fund will also struggle to maintain pace with Bitcoins appreciation due to scarcity. Stocks, real estate, and bonds - are all instruments priced in fiat currency today. They all should have soft potential price maximums. Referring to the previous section, a bet on say the stock market versus Bitcoin over the long term, is a bet on equities ability to continue to grow by hundreds of trillions of dollars, compared to Bitcoins ability to grow from it's current size to 5 trillion, and then 10, and beyond. Bitcoins theoretical market cap will be reached when it has consumed every single unit of fiat currency. The question should be, what sectors or asset classes will be poised to outperform Bitcoin, when they are all paid for and priced in the money which is simultaneously leaking value and they already compose huge chunks of the global asset market? Risk Hedge - today Bitcoin trades in high correlation with the stock market. This is a conversation about long horizon time planning. The same argument about reduced volatility over time, should lead to an at least corollary argument that Bitcoin will eventually also decouple from tech stocks. 5 Countries & Governments currently own Bitcoin, it's future likely is to be held by many more. https://www.buybitcoinworldwide.com/treasuries/ In this case the best way to think about it is, how do we view the long-term performance potential of the stock market, against the inflationary pressure created by necessitated money printing. My guess is that over time traditional assets will be a riskier bet, than a single transparent network that has a permanently fixed number of units. Again we are looking at this from the lens of long-term assets to build your portfolio for retirement around. Which would you rather place a 20 year bet on today? The fastest growing, most viral technology in human history - which is built on planned scarcity? Or an increasingly risky mix of equities required merely to outrun prolonged inflation? What are some possible paths to incorporating Bitcoin into a pension strategy? Holding BTC inside a pension. It's happening already. The Houston Firefighters’ Relief and Retirement Fund (HFRRF) announced in 2021 that it was investing $25 million in bitcoin, the first time a U.S. pension fund invested in cryptocurrencies. Bitcoin is digital property. The idea of property being digital is new a concept to wrap your head around, but physical property has long been a stable of pension funds. The basic concept of holding BTC in a pension is not as absurd as you might think. As an alternative in Canada you might be have the ability to allocate or self direct pension funds into a Bitcoin Exchange Traded Fund like Purpose Bitcoin ETC - trading as BTCC. Bitcoin ETFs hold Bitcoin as the only underlying asset, and so while you don't get the benefits of participating in owning actual Bitcoin going this route, you will from a retirement planning perspective enjoy the long-term price appreciation of the scarcest asset in the world. In the absence of either of those options holding Bitcoin outside of your pension, as a tool to offset the long-term inflation risk to your benefits. Bitcoin as a parallel investment for those counting on pensions, offers insurance against the erosion of the real world value of pension benefits. Custody of actual Bitcoin scares many but is always preferable to an investment in a product where Bitcoin is the underlying asset. This will be more and more evident over time. Digital assets are a new idea today but this attitude will pass. Possessing and storing your own Bitcoin is more secure, keeps them more liquid, and prevents any possibility of seizure or confiscation. Bitcoin is a novel, and maturing financial instrument. We need to start thinking about how to incorporate it into the existing framework of retirement planning. I believe it is the apex predator of inflationary monetary policies, which pensions and pensioners are especially vulnerable to. About the guest author - Scott started in the insurance industry in 2008, holding various sales leadership roles with Canada Life before becoming an advisor in 2016. In 2022 he made the decision to transition to the world of Bitcoin and in his current role with Bitcoin Well he is using his experience in traditional financial services sales to help Canadians and Canadian Companies make informed Bitcoin purchases. Scott is a Bitcoin enthusiast and a graduate of Wharton Business Schools Economics of Blockchain and Digital Assets. s.dedels@bitcoinwell.com Note from The GAB - this website is not giving advice. When incorporating cyrpto (or doing any investing outside of an RRSP or TFSA) into your retirement plan, please consider the taxable nature of any gains made in this volatile marketplace. Never invest more than you're willing to lose. 6/4/2022 GUEST POST! 3 significant forces that will reshape the talent landscape in Canada for yearsRead Now A Business Development Bank of Canada Study – Future-Proof Your Business – identified three significant forces that will reshape the talent landscape in Canada for years to come:

Demographic complexity makes it much more challenging to assist employees in obtaining knowledge and information to help them better understand their current financial situation and gain peace of mind. In today’s changing financial landscape, managing a workplace financial program – whether the purpose is for retirement or savings – is an important responsibility. It is also undoubtedly difficult to devote the time to with many conflicting priorities vying for attention. Organizations are faced with ongoing volatility, mounting uncertainty and inflationary costs, not to mention the time it takes to manage their programs properly. Combine this with the lingering concerns from the pandemic and its overall impact on the emotional and financial health of their organization, their employees, and their HR teams, it is becoming clear that the compensation picture is becoming more difficult to manage. With an eye towards the future, here are 3 trends that are we seeing progressive employers explore with respect to their group retirement plan designs. 1. Flexibility, Flexibility, Flexibility Similar to health benefits, employees are looking for flexibility to address various financial needs. These needs may fall outside the immediate scope of retirement but will ultimately play into one’s ability to save over the long term:

2. Women in the workplace The impact that the pandemic has had on women in the workforce is well documented. According to Sun Life’s 2021 Designed for Savings Report, the average account balance for men exceeds women across all industry sectors. The lower savings levels are due to lower on average earnings* and some systemic plan design features. Plan Design Considerations: Review eligibility rules and leave policies with a female lens Many retirement programs still have a 12-month waiting period to join the plan. Women also take parental leave more often at which point their ability to save is put on pause. A mother with two children who has had to make 2 job changes over her career to balance the family, could easily have 3 or 4 less years of workplace savings than her male counterpart due to rules that have been in place for generations 3. Designing communication strategies that focuses on the needs of people The standard “one size fits all” communication approach doesn’t really work for employers with today’s multi-generational and multi-cultural workforce. Organizations that approach their communication strategy using demographic data and cultural realities have a greater chance of ensuring employees have opportunities to improve their financial mental health which can become a competitive advantage: Plan Design Consideration: Design a communication strategy around the four generations in the workforce and those newer to Canada

What are you doing to address these forces and what trends are you seeing? Thanks to Paul Webber for this guest post! Paul leads the Group Savings and Retirement practice at Green Benefits Group where he brings over 30 years of experience as both a plan sponsor and a consultant. So he knows a thing or two about retirement and savings trends! If you want to chat more with Paul about this or other things, you can find him on LinkedIn and via the classics: phone 416-565-6955 email p.webber@greenbenefitsgroup.ca Gotta cite those stats *In 2018, females aged 25 to 54 earned $0.87 for every dollar earned by men on an hourly basis according to The gender wage gap in Canada: 1998 to 2018. Statistics Canada, October 2019. Back in 2017 the waiting period for EI was shortened from two weeks to one week. There was no change to the claim duration.

What did this mean for short and long term disability benefit plans? For short, employers participating in the ei reduction program just needed to make sure their waiting period was still in line. For LTD it meant plans with a 120 day waiting period would have a week long gap between ei ending and Ltd beginning. Many employers did not reduce the waiting period to realign with EI and employees still have a gap week with no income. And we still commonly quote 120 day waiting periods. This does shift some cost to the employee. Today Bill C-30 is proposing more changes to EI that will impact the Disability benefit. This time the claim duration is being impacted. The plan is to increase the duration for sickness benefits from 15 weeks to 26 weeks. There is currently NO go date for this update. And the government has not shared how this will affect the ei reduction program. What should you do? This is a good time to start planning so you’re ready when the changes do (if ever) go into effect. Will you want to update your disability plans to align with EI? What is the impact to individuals from a claiming and cost perspective? Will long term disability plans begin to separate sickness and injury? What scenarios need to be thought through with this possible change? 10 Free Mental Health Resources for Canadians. What are they for? Where to find them? How to use it?

May 2-9 is mental health week. Get your tool kit here. Now into the list – 10+ free mental health resources for Canadians 1. Wellness Together provides mental health and substance use support for people in Canada and Canadians abroad . It’s a 24/7 free virtual resource run by the Government of Canada. In this site you can search for written resources, talk with a councilor over the phone, or create an account to access courses, apps and more. 2. Anxiety Canada – is a registered non-profit organization, created to create awareness about anxiety and support access to proven resources and treatments. They have free online, self-help tools to help manage anxiety. You can use anexiety Canada’s free CBT (cognitive behavioural therapy) app MindShift, to a group therapy program that can be claimed in your benefits program, or use their step by step online course for anxiety management. 3. Bounceback is a free skill-building designed to help adults and youth 15+ manage low mood, mild to moderate depression, anxiety, stress or worry. Delivered online or over the phone with a coach, you will get access to tools that will support you on your path to mental wellness. 4. PocketWell app – by the Federal Government program Wellness Together Canada. Track your mood and well-being and access mental health & substance use support from professional counsellors. All services are free, offered virtually or over the phone. you'll be able to use research-based tools to measure and track your well-being, including a Self-Assessment developed by psychologists. The Mood Meter will also let you keep a log of how you’re doing through quick daily check-ins. ONE-TO-ONE SUPPORT From the app, you'll also be able to connect with trained counsellors & crisis responders who can talk to you about what you're going through and help you through intense situations. Send a text message or call one of WTC's phone counselling lines any time of day or night to get support, available anywhere within Canada. 5. Crisis Services Canada /Talk Suicide Canada– Need help? Connect with a person at the Canada Suicide Prevention Services. If you’re thinking about suicide, are worried about a friend or loved one, the Canada Suicide Prevention Service is available 24/7/365 for voice and 4pm to 12am EST for text. Call 1.833.456.4566 Text 45645 6. Kids Help Phone offers e-mental health services are available 24/7 across Canada. This means that we’re here for kids, teens and young adults from coast to coast to coast. They offer mental health tips and info. Crisis support and counselling over the phone or online. Call 1.800.668.6868 Text 686868 7. Workplace Strategies for Mental Health – This one is a bit different. They provide strategies, approaches and workshops for organizations and people leaders, along with practical resources for employees on topics including emotional intelligence, dealing with a stressful boss, resolving conflict and more. Everyone can benefit from the tools on this site. CMHA National – the Canadian Mental Health Association has local chapters that can help you. The CMHA can help you find resources and your local chapter will have local resources. 8. Heads Up Guys – health strategies for managing and preventing depression – for Men. They also have a therapist directory. 9. The National Standard of Canada for Psychological Health and Safety in the Workplace (the Standard) – the first of its kind in the world, is a set of voluntary guidelines, tools and resources intended to guide organizations in promoting mental health and preventing psychological harm at work. 10. SmilingMind is a free meditation app and a not for profit.. I’m sure there are others, this is the one I happen to use. Province specific: BC – A hub of mental health resources – free, low cost and more for residents of BC. A more robust list than what I have made! Togetherall a safe, online community where people support each other anonymously to improve mental health and wellbeing. Millions of people across Canada have free access through organizations, colleges and universities. Togetherall is free to all Alberta and Nova Scotia residents aged 16+ Good2Talk provides free, confidential support service for post-secondary students on NS and ON Other: Cognitive Behavioural Therapy Programs like those offered by MindBeacon, Anxiety Canada and AbilityiCBT can be claimed through the psychology benefit in the group benefit plan. Actively at Work - The employee is at work for the employer (not disabled or on leave). Detailed definition is included in the group contract. AD&D - Accidental Death & Dismemberment - pays for accidental death, or for loss of limb, eyesight, etc. Agent of Record - The Agent of Record is the advisor appointed by the plan sponsor. An AOR letter is required on the plan sponsor’s letterhead in order for the insurer to pay commission and to release information to the advisor. ASO - Administrative Services Only - a non-insured plan where the Employer is paying for all the claims plus an administration fee for the Insurer’s claim payment services. Assignment – When used in the context of health or dental claims, it means the employee can “assign” payment to the Insurer. This is done, for example, with a dentist so that the dentist can bill the Insurer direct and not require payment up front from the patient. Anti-Selection – A situation where only the individuals in poor health join the plan and health individuals do not; where the option is available for employees to opt in or out; the smaller the group, the less “choice” there needs to be to avoid anti-selection. Benefit or Benefit Amount - More correctly called the “volume”, this is the amount of insurance. For example, an employee insured for $50,000 of Life insurance has a benefit of $50,000 or a volume of $50,000. CI - Critical Illness Insurance – pays a lump sum tax free amount to the insured on diagnosis of serious illness such as cancer, stroke, etc. Class – When referring to employee benefits, “class” is a group of employees that have identical benefits. Example: Class A could be Executives, Class B could be Office Staff, and Class C could be Yard Workers. Each would enjoy a different level of benefits. COLA – Cost of Living Adjustment - usually a benefit that can be added to Long Term Disability, it allows the benefit to increase each year based on a defined formula that is usually tied to CPI (Consumer Price Index). CPP - Canada Pension Plan (and QPP Is Quebec Pension Plan). Conversation Privilege- Contractual right for plan members to apply to replace group coverage the lose with individual coverage without a need to submit evidence of insurability. COB – Coordination of Benefits - This clause helps insurers determine the order of payment when both the employee and the spouse have group insurance through their employers. COB order is as follows:

Cost-Plus – is a Private Health Services Plan. This is an arrangement to provide a facility for payment of legitimate expenses as listed by the income tax act under the medical expense category. When used in reference to offering health or dental benefits, is a facility to have the employer pay for health or dental expense, and pay an administration fee for the privilege. Running the expense through an Insurer creates a tax-free payment to the employee. If the Employer were to reimburse the employee directly for the expense, then it would be considered “salary” and would be taxable to the employee. Credibility - Degree of reliability that the group's own experience can predict future claims. DEN – Dental Dependent - Members of the employee’s family who are eligible for benefits. DIN - Drug Identification Number (shows on prescription receipt). DPL - Dependent Life Insurance - nominal amounts of life insurance on an employee’s spouse and children. EAP / EFAP - Employee & Family Assistance Plan - provides confidential counselling or resources to employees and usually their family members as well. EHB - Extended Health Benefits - Coverage for health expenses incurred by the employee (and his dependents if applicable) not covered by the provincial health care plans such as semi-private hospital, prescription drugs and medical services and supplies. EHC - Extended Health Care - means exactly the same as EHB. EP3 Statement - Certificate issued by the insurer to confirm the drug plan is eligible for national drug industry pooling and is protected by the insurer's Extended Drug Policy Protection Plan pooling. EP - Elimination Period (used with Long Term Disability). This refers to the waiting period an employee must be totally disabled before LTD benefits become payable. “Evidence of Good Health” – Refers to a medical questionnaire an employee must complete to disclose medical history. Also referred to as “health evidence”, for example: “the employee must supply evidence of health…” Experience - Certificate issued by the insurer to confirm the drug plan is eligible for national drug industry pooling and is protected by the insurer's Extended Drug Policy Protection Plan pooling. Generic Drugs - Generic drugs contain the same active medical ingredients as the corresponding brand name and there therefore considered therapeutic equivalents. Generic products generally cost less and if purchased instead of brand name drugs, can reduce drug plan costs. Grandfather – In insurance terms means taking on the same level of benefits as an employee had with a previous carrier, so that the employee does not lose benefits. This is standardly done for Life and LTD. It is important an employee not use a valuable (and possibly irreplaceable) benefit because the employer changed Insurers. See also the term “takeover”. Gross or Net Rates - Net rates are the premium rates charged by the Insurer; gross rates are the rates the TPA charges the client. The difference is the TPA’s commission and fees. HSA or HCSA– Healthcare Spending Account – A healthcare spending account is a fund of money provided to employees by the employer. The employee can use these funds to pay for anything that CRA has deemed a medical expense. Employers pay an admin fee, that may or may not include commission to the HSA provider to administer the claims IBNR – Incurred but not Reported - The insurer is required to set funds aside to fund claims that may be made but are not yet known to the insurer, in the event that the plan terminates. It is most often a per cent of claims. LAP – Large amount pooling – pooling – stop loss - Level over which a plan member's claims are directed to a pool with other large claimants and replaced by a pooling change to reduce claims volatility. Late Applicant - Eligible plan member who applies to join the plan after the application period (usually 31 days after becoming eligible) has expired. LTD - Long Term Disability - A monthly insurance payment made to a disabled employee after a period of illness or injury. Medical Evidence - A health statement an employee completes to show he is in good health. The Insurer reserves the right to order other medical evidence as a result of what is disclosed on the health statement. MGA – Managing General Agency – an organization that does back office work for financial advisors and group benefit advisors. NEL - Non-Evidence Limit – maximum amount of insurance an employee can receive without medical evidence of good health. NEM - Non-Evidence Maximum – exactly the same as NEL. Net Rates or Gross Rates - net rates are the premium rates charged by the Insurer; gross rates are the rates the TPA charges the client. The difference is the TPA’s commission and fees Non-Smoker – Has not used any tobacco products at all (including snuff, marijuana, Nicorette gum) for 12 consecutive months. NOTE: Voluntary (optional) benefits may include smoker/non-smoker rates, however basic group insurance benefits do not, and employees are not asked if they are smokers unless applying for excess coverage or optional coverages for which they are eligible to apply. NPC – No prior coverage - a group that has never had a group benefits program. OL - Optional Life Insurance – an employee may purchase additional insurance, with medical evidence (that is, a health questionnaire). OM- Overall maximum – the maximum insurance an individual can apply for, even with medical evidence. OOC - Out-of-Country - refers to being covered for Extended Health while traveling outside Canada. Paramedical Services – Chiropractor, psychologist, massage therapist, naturopath, speech therapist, and more (covered under Extended Health). PDD - Pay-Direct Drug Card - use it at the pharmacy and the pharmacist can bill the insurer direct. Plan Member - An employee or their dependent who are covered under a group Plan Sponsor - The Employer who holds the Group Insurance contract Pre-Ex - Pre-Existing Condition Pre-determination of benefits - An estimate submitted by a dentist for certain major dental expenses (such as crowns, bridges, dentures or braces) before the dental work begins. Preferred Provider – the Insurance Companies an advisor prefers to deal with. Provider - Insurance Company/Insurer - occasionally the insurer is called the “underwriter”. R&C - Reasonable and Customary - if a benefit has an R & C limit it means the insurer doesn’t name a limit in the contract but would not pay unlimited amounts for an expense. The reimbursement would be limited to what the insurer considers reasonable. Rate (or unit rate) - multiply the rate by the volume (benefit) to get the premium. Renewal Date – The policy anniversary. Group Insurance contracts usually renew one year after the inception date, although occasionally the first renewal will be longer (e.g. 15 months). Once the policy has had its first renewal it will renew annually thereafter. For example, if a plan has a renewal date of September 1, then the rates are subject to change (renew) September 1 every year. RFP / RTP / RTQ - Request to Quote - Facts submitted to the insurer on a group prospect by a licensed adviosr in order to obtain a quotation. SIC – Standard Industry Code – a list of business categories compiled by Dun & Bradstreet (in the US) or Stats Canada (in Canada). Most Insurers use D&B. A code is assigned to each business type. Example: 8600 would be Health; 8620 is non-hospital institutional health services; 8663 is Practical nurses. Code 6300 is Retail; 6311 would be auto dealers, 6330 gas stations; and so on. STD - Short Term Disability - pays an employee an income while unable to work due to accident or sickness. When used in the world of Group Insurance it hardly ever means “sexually transmitted disease”. Takeover – Refers to “grandfathering” of benefits as in, “we will take over your existing benefits with no loss of coverage”. Legislation requires this of all Insurers for Life and LTD. A copy of the prior Insurer’s billing statement must be sent to the new Carrier to ensure no employee loses coverage. NOTE: some Carriers have limits as to how much benefit they will take over, and will refuse to take the case if those limits are exceeded. Underwriter – is another term for the Insurer, although it is not commonly used. Another definition of Underwriter is an employee who works in the Underwriting department. This department is responsible for assessing whether a risk is a good one, deciding whether an exception can be made on rates, provision of benefits, or liberalizing the rules if the reason for the exception makes sense. TLR – Target Loss Ratio - Portion of the premium that is used to cover the projected claims, equals 100% - expense level in % of premium. TPA – Third party administrator – an organization that does billing and administration TPP – Third party payor – an organization that pays claims. Not an insurance provider. Trend - Level by which that claims are expected to grow due to price inflation, increase in utilization, introduction of new expensive treatment TSA - taxable spending account, aka wellness spending account - Just like the healthcare spending account, the TSA is a fund of money provided to employees, paid for by the employer. Just like with the HSA, the employers pays an admin fee to the provider to administer the claims. With the TSA employees can use it for literally anything. Yes anything. Most providers will set a contract with the employer to narrow down anything to most things, divvied up into categories to help drive employee behaviour with a goal of health and wellness in mind. These are commonly used for fitness memberships and sports equipment. It can also be used to buy insurance products like optional insurance, pet insurance and virtual care Underwriting - The process of assessing risk and determining the required rates for the group. Vol. AD&D - Voluntary Accidental Death & Dismemberment - the terms “Voluntary” and “Optional” are interchangeable - usually available to both the employee and the spouse, and sometimes on the children as well. Volume of Insurance - the amount of insurance an employee is insured for. If his Life is $50,000 then the volume is $50,000. This can also be called the “benefit amount” Waiver of Premium - When an employee becomes disabled, his life insurance premium may be waived for the duration of his disability. WI - Weekly Indemnity or Weekly Income - means exactly the same as STD Important note about calculation of benefits: Life Insurance and AD&D are rounded up to the next highest $1,000 if not already an even multiple of $1000. WI and LTD are rounded up to the next $1.00 if not already an even multiple of $1. Life, AD&D, WI, and LTD unit rates are usually rounded to 3 decimal places. Dependent Life, Extended Health, and Dental are 2 decimal places, since all are a “cost per person”.  Will the national dental plan save me money on my employee benefit plan?

In short – probably not. Not right away anyway. This what we know about the dental plan today. It will start with those under 12 years old some time in 2022. In 2023 the program will expand to those under 18, seniors and persons living with a disability. By 2025, the program will be fully implemented. The program is income restricted. Families with an income of less than $90,000 will be eligible and only those with an income of less than $70,000 will not pay anything. Let’s break this down. Here’s what we don’t really know yet. First – a lot of services fall under dental care. Everything from cleaning your teeth, to fillings, to crowns, to braces. What will the government cover? At the point of writing this, we have no idea. I suspect it will be basic coverage. Second what does fully implemented mean? Does that mean all Canadians making a family income of less than 90,000? The income threshold seems to be aligned with the median family income in Canada, which is $90,390. Will this amount be adjusted annually to keep up with wage changes in inflation? Third – How will this program interact with insurance plans? Will more details reveal that the program is only for those without insurance? Will the program coordinate with insurance plans? Will the national dental program pay first, before an insurance plan pays or will it let the insurance plan pay first? You’re probably thinking, but coverage for 12 years old and younger is starting right away. Won’t that save the employee benefit plan money? It will, but probably not a lot. Here’s why. About 15% of the total population is aged 0-14 years old. That’s a pretty decent amount of the population. But many of those years’ kids don’t see the dentist. Plus (with the exception of braces) the work kids are having done mostly falls into the basic dental category which costs a lot less than crowns, caps, implants and other major work that happens as we age. Let’s dig into this income cap that limits coverage eligibility. This is what will exclude most people from qualifying for the plan. The national dental program is only for people who have a family income of $90,000 or less. Key word here is family. A family income includes the incomes of everyone in the family which in most cases is the two adults. In 2015 69% of families had both parents working aka dual income. In Canada the median family income is $90,390. Median is different from average. Median is the middle – it means that half of Canadian families make more than $90,390 and half make less. Using the median income in Canada to qualify for the plan, means half of Canadas will not be allowed to use the national dental care plan. Of the half that are able to use the plan, many will still have to pay to use the coverage. Only those with a family income of less than $70,000 will not have to pay anything for the plan. Again, we don’t know what will be covered in the plan. What about coordination? How will the new national dentalcare program interact with insurance plans. We don’t know. With drugs, the system to coordinate with provincial coverage is already set up. For dentalcare a new system will need to be set up for dentists to submit claims to the government plan for reimbursement. Insurance carriers and dental offices will need clarification on the order of payment. In insurance there is something called a first payor. The first payor is the main source of insurance coverage and where the dental office will submit claims first. After the first payor has refunded the dental office for the claim if there is any cost left to pay, and the individual who had the dental services has other coverage that plan may pay for the services. Or if there is no other coverage available then the individual will pay. No matter what or who the new national dentalcare program covers, employers will save money. But employers should not rush to reduce or remove dental coverage until we know the unknown. With dental costs on the rise, and turnover at an all time high, employers should stay on track with their benefit program updates. Once more is known about the plan, we can make smart decisions on what to change, if anything about the dentalcare portion of the employee benefits plan. *most of the stats in this article are from Stats Canada. The google machine will find them for you if you ask nicely. 4/11/2022 5 reasons why employers should NOT pause benefit plan updates because of national pharmacare and dental care announcementsRead Now 5 reasons why employers should NOT pause benefit plan updates because of national pharmacare and dental care announcements:

1. The dentalcare program won’t be fully launched until 2025 if it keeps to the proposed timeline. 2. The dentalcare program has a household income limit of $90,000. This means most employees will not qualify for the program. 3. Pharmacare wasn’t given money in the 2022 budget and will take a long time to launch anything. We have no idea what this program will and will not cover. 4. Drugs and dental costs are rising now and are not slowing down. If you were planning on making plan changes that will help reduce your drug risk, you should still do those. 5. Employee turnover is at an all time high and will continue for the foreseeable future. Group benefit plan enhancements can help you win and keep employees. Let’s dig into employee benefit plan updates a little more. The 2021 Driving Data with Decisions – Benefits Strategy and Benchmarking Survey by Gallagher found that 62% of employers have no plans to update their benefit program. In fact, most benefit plans haven’t had an update to the drug plan in over a decade. Why are employers setting and forgetting something that costs anywhere form 5-15% of payroll? It’s all about change – people hate change and if it ain’t broke, don’t fix it. But I would argue that benefits are broken to an extent. Plans we put in place and haven’t updated a decade ago don’t address today’s concerns. Digital, personalized, risk, cost. These have all evolved. Employees want a personalized benefits experience, one that meets their needs (wants) now and in the future as their lives change. Most people, also have a case of the “that won’t happen to me’s” which means employers will need to consider how much they listen to what employees want. To decide what part of the plan to update, and if they should update the plan at all, employers should start by answering this question – what is the purpose of the employee benefit program? Is it a tool to recruit employees? Is it something they just have to offer? Is it a tool to protect employees from expensive life events, like a disability or chronic condonation? Is it a tool to keep employees healthy? From there employers can determine how much they can afford to pay for the plan now and in the future. Once an employer understands what they want to accomplish with their group benefits, they can update the group benefit plan. A few items that all employers should consider as they decide on what updates to make are:

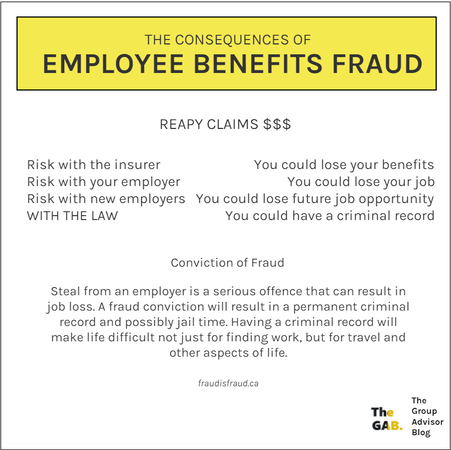

Employee benefits fraud is the real deal. When someone - an employee or provider commits benefits fraud they are stealing from the employer who offers the group benefit program - NOT the insurance carrier.

The consequences of benefits fraud are like the cards in the game of Monopoly. You don't get to pass go and collect your $200 because you're fired. Stealing from your employer is a serious and fire-able offence. This can also make it difficult to find a new job. If you're lucky you'll land a get out of jail free card. Even if you do, a fraud conviction results in a permanent criminal record. A permanent record will make doing fun things like travelling difficult. You could also have difficulty getting a job and achieving other life goals like buying a home. Like the community chest card - you'll still have to pay your doctor's fee. Those who commit fraud could be responsible to repay the stolen money. Not committing benefits fraud is easy and you can learn more at fraudisfraud.ca I read a stat from the Envoy Return to Workplace Report that reveled 63% of employees say flexibility would make them feel more empowered. The 2020 Benefits Canada Healthcare Survey shows how much value plan members place on having some control over how they can use their health benefit plans.

Personalizing benefits is key to unlocking an engaged workforce. The definition of personalized is “design or produce (something) to meet someone's individual requirements”. Personalizing benefits gives employees the flexibility and control they need. I participated in a couple of webinars last week that focused on plan member personalization. Below are some the stats that make a compelling argument to giving plan members more flexible benefit options.

The top 4 products that plan members would like to use if added to their benefit plan can be delivered through a taxable spending account (Fitness Classes, Personal fitness trainer, Virtual Care, Fitness tracking devices). BUT The Gallagher Driving Data with Decisions Survey found that 62% of plan sponsors have no plans to make updates to the benefit program. The great reset is on. Headlines are 40% of employees say they are at least somewhat likely to quit in the next three to six months. Mass attrition is happening. It’s widespread, and will persist for the foreseeable future. Stale, outdated plans from a decade ago, that try to fit everyone into the same tiny box, push great people out the door and open the door to disrupters and to competitors. 2/14/2022 Should Employee Benefit Providers embed “value add” products inside the healthcare rate?Read Now Should Employee Benefit Providers embed “value add” products inside the healthcare rate?

This is kind of a big and loaded question because whether or not they should, they do. It’s common practice. I will admit that my opinion has evolved over time. I used to think of products embedded in the healthcare rate as a value add and as insurance carrier differentiator. But not anymore. How can a product add value if it’s not wanted? Then it becomes a takeaway. When employers are not given the option to opt out of these so-called value adds, and when the cost is hidden it becomes problematic. Some quick disclosure, over at my day job, my employer and insurance carrier Equitable Life doesn’t embed costs. But my opinion on this was actually reshaped when I was working on the advisor side of our business. Multiple billing wasn’t as big a deal as I thought it was and the admin liability risk on forgetting to add someone to the wellness program is low. Plus these providers do a great job making set up and ongoing admin a breeze. Way back in 2006 when I joined the wonderful group benefits industry the costs hiding in the healthcare rate were limited to the pooling charge and Best Doctors. Best Doctors is the OG value add. If my memory serves me well, the cost was around $0.50 for a single and $1 family. But today hidden costs have ballooned to include the second opinion program, HR tools, wellness (like lumino and vitality) EAPs, virtual care and more. All of these programs have a cost. So who cares? What’s the big deal? Benefit plans are under pressure. Drug risk is high, disability is suffering from prolonged historically low interest rates coupled with longer duration periods and higher incident rates. Dental fee guides are increase 5-7%. Higher cost is everywhere. These embedded programs could cost an employer anywhere from $1-$5 per person. Since well all like percentages, that could be as high as 10% of the single healthcare rate. Imagine if your clients had an extra 10% to spend? Here's what else an HR department could get for $1 - $5 per person

The list goes on. The other problem is that it complicates future cost forecasting. The cost for the add on products is backed out of the healthcare premium in renewal calculations. You can’t quick and dirty math your way into a three-year cost prediction. In addition to backing out the pooling charge you now have to dig into how much do each of these add ons cost. I’m not a fan of this lack of transparency. Instead, why don’t we price each of these options and let employers choose if they would like to offer the program to their employees? Not all employers want these services tied to their insurer. It creates additional change management for employees. New insurer, new EAP, new virtual care, new wellness. It’s too much. What do you think? Should third party services be billed in the health rate? Should they be mandatory or optional? |