Let's all promise to make meaningful resolutions this year that we can keep. With that in mind, I give you, group benefit resolutions for the advisor, plan sponsor and plan member!

Plan Advisor

In 2017 something exciting happened. GSC Canada launched a podcast. It was the first employee benefits podcast that I listened to and now I can't get enough. Since then a number of podcasts have launched. Some have come and gone, others evolved and some have thrived. Here is a list of my favourite (alphabetically!) mostly benefits related, some fintech related podcasts.

Have I messed any?! Add them to the comments. You'll find these where you listen to podcasts!

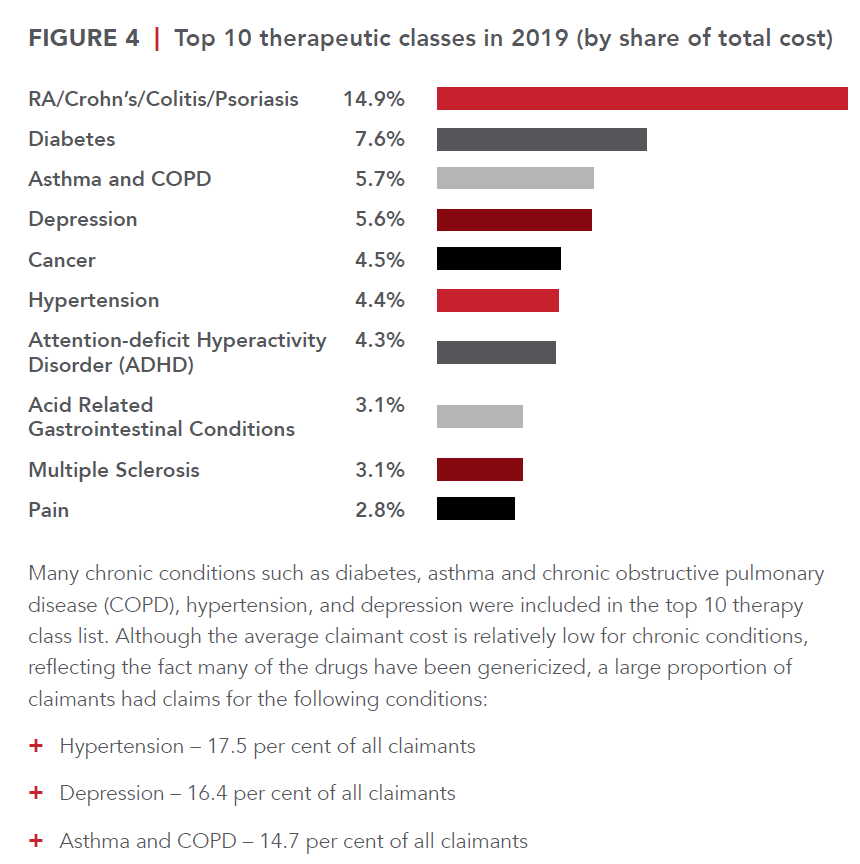

Bonus: US based with relevant general topics like how to make decisions with discernment is Benefits Influencer with Ned Schaut 12/6/2020 I Read it, So YOU Don’t Have To the 70 page goodie from HBM+: 2020 Drug Trends and Strategic InsightsRead Now  In this episode of I Read it, so YOU Don’t Have To is the 70 page goodie from HBM+: 2020 Drug Trends and Strategic Insights. You can access this report here. I recommend viewing the many visuals and reading the section on drug formularies: page 44-48. Ready?! Let’s dive in. Who is HBM+? One of the largest pharmacy and health benefits managers in Canada, HBM+ is a division of Green Shield Canada. The data presents drug claims and utilization data for their six partner insurers and third party administrators (TPAs), representing over two million claimants, and over $1.5 billion in annual adjudicated drug cost. These are their insights (peppered with my commentary of course). If you have read any drug claim report in the past, you’re familiar with what’s about to come. Drugs costs are rising, high costs drugs are a problem. Etc, etc. So here it is again. Only this time, let’s take action after reading this. Since 2014 drug trend ranges from 4 to 14.2% (taking out the OHIP+ blip year where the Liberal government shifted all drug claims for those under age 25 to the province only to have the Ford government quickly reverse that initiative). The average drug cost per claimant rose from $61.90 in 2015 to $66.00 in 2019. Not noted here, but in other reports is the dramatic difference between the average provincially. This highlights how well provincial drug programs reduce the cost burden on employers. Atlantic Canada has by far the worst average drug cost per claimant and this is directly related to their lack of provincial drug coverage. The average annual cost per claimant for the top 5% was $8,306 in 2019, which was more than 21 times that of the other 95% of claimants ($392). The top 5% of claimants had an average of 66 claims in 2019, versus just nine claims for the other 95% of claimants. The top 1 % of claimants have an average annual cost of $24,740 which is 31.4% of the total drug costs. This is where we can get a lot of bang for our buck with biosimilars (and a drug formula plus provincial drug plan alignment). Many of these high cost drugs are not just biologic claims, but originator biologic claims. Call to action: Group Benefit Advisors must begin to have proactive risk conversations with employers around biologic drugs. As we see the provinces delisting many originator drugs, not all carriers are following suit making this the risk conversation with employers vital. When an insurer does not also delist a biologic drug, it puts additional risk and unnecessary claim pressure on employers. BC has already delisted a bunch of originator biologics Most insurers in BC also delisted, but a few held out forcing employers to pay for these expensive drugs when the provincial program should have picked up the cost. More on this in the biosimilar section. Generic drugs have been and continue to be an important source of savings for drug plans. Generic penetration rose to 62.5% in 2019 from 55.3% in 2015. There is room for improvement. Call to Action: If your plan doesn’t already have a lowest cost alternative or mandatory generic substation built into it, what are you waiting for? Do like to spend more for the same product? The generic price negotiations between Canadian Pharmaceutical Alliance (pCPA) and the Canadian Generic Pharmaceutical Association were key. For some generic molecules, the price was reduced to as little as 10% of the brand-name equivalent They say a picture is worth a 1000 words. I think this graph speaks for itself. While the top drug category is concerning and cannot be ignored, there’s a lot we can do to reduce claims with a healthy lifestyle in other categories. The average cost per claimant for diabetes is $981 and there are 119,168 claimants. While hypertension has almost 350,000 claimants with a cost of $197 per claimant. We can make significant improvement to claim costs if we proactively tackle these conditions. Call to Action: what proactive plan design is in place to promote health? What wellness initiatives are built into the employee’s experience? In 2019 18,200 claimants used a specialty drug. This represents growth of 11.2% over 2018. This is not sustainable and represents a huge risk to benefit plans. The arrival of biosimilars offers incredible opportunities for savings while maintaining plan member access to effective drug therapy. Another cost management strategy that has been successfully employed to manage specialty drug expenditures is preferred pharmacy networks (PPNs). PPNs are an important tool to manage the pharmacy markup of specialty drug claims. As specialty drugs can cost over $100,000 per year, the pharmacy markup represents a substantial sum of money. PPNs are structured to not only reduce the standard pharmacy markup for these claims but also bundle additional value-added services such as adherence support and case management. When combined, these programs can control claim costs and ensure patients are appropriately using these high-cost therapies. Pharmacy Listing agreements are equally essential in the management of specialty claims. Since 2010, the pan-Canadian Pharmaceutical Alliance (pCPA), has utilized the collective buying power of the provincial drug plans (and the federal government) to negotiate drug prices for over 200 drugs. As of March 2019, the pCPA has been able to realize savings of over $2.26 billion annually. This effort has substantially enhanced the sustainability of public drug plans across the country. No such collective buying effort currently exists in the private sector. Shifting the cost of a high cost claim from the employer, to the public pan whenever possible is a key strategy for employer drug plans. Since 2014, 10 biosimilar products impacting private drug plans have been approved and marketed in Canada to treat a range of different conditions, including diabetes, Crohn’s disease, psoriasis, and neutropenia. Biosimilars present comparable safety and efficacy to their originator products, but at a significantly lower cost; in fact, the discount attributable to a biosimilar relative to a reference product is over 50% for some products. As private drug plans embrace biosimilar-first policies and biosimilar transitioning, biosimilar penetration is expected to grow substantially in the coming years. The benefits of these therapies for private drug plans extend beyond immediate cost savings, translating into better integration with public plans, many of which are starting to implement biosimilar switching policies. In particular, in 2019, British Columbia became the first Canadian province to implement a biosimilar transitioning program for all Residents that led to substantial savings for the public drug plan without compromising patient safety or access to drug therapy. Since then, Alberta has also announced the implementation of a biosimilar switching policy, and it is expected that Ontario will make policy decisions to move forward with a similar approach. Call to action: talk to employers about the risk of being insured by a carrier who has not also delisted these drugs. Most chronic disease sufferers claim for maintenance drugs on an ongoing basis, after initial effectiveness is established. It follows that maintenance drugs should be dispensed at three-month intervals to facilitate patient adherence and reduce overall dispensing fee costs. In 2015, 90-day supply claims made up close to 28% of the total number of claims As a result of the implementation of the maintenance medication dispensing frequency policy in 2016, the share of 90-day supply claims rose steadily over time before stabilizing at around 40% in 2019. In that same time, claims for 30-day supply dropped from 19.9% of the total number of claims, to only 10.5% Opioid management is an important topic since there is an epidemic of opioid overdoses. HMB+ notes that the issue is extremely completed and cannot be solved by one stakeholder alone. It will require a concerted effort among multiple partners, including health care providers, insurers, TPAs, advisors, plan sponsors, and pharmacy benefit managers. They go on to describe their three-component opioid management policy: focus on abuse deterrence, restrictions on long-acting formulations, and opioid medication utilization reviews. Implementation of this policy instantly lowered the number of claimants using oxycodone from about 160 in May 2017 to just 10 claimants in July. The drop in the number of claimants eventually stabilized at an average of just 17 claimants monthly in 2019. Managed formularies are one of the most effective, yet underutilized tools to drive value and cost containment. Managed formularies are based on the premise that drug prices are not always commensurate with the level of therapeutic value they deliver. This is supported by analysis undertaken by the Patented Medicines Price Review Board (PMPRB). Based on a 2017 report from the PMPRB, 82% of new drugs that entered the Canadian market between 2010 and 2017 were classified as offering little to no improvement over existing therapies, and only 5% were classified as breakthrough or had a substantial improvement over existing therapies. With this understanding, managed formularies are designed to bend the curve on drug spending by proactively encouraging the use of the most cost-effective treatments that generate value for both plan sponsors and plan member Under an open formulary, non-high-cost drugs approved by Health Canada are covered regardless of their cost or whether or not they provide any meaningful value over existing therapies. In 2019 79% of claimants belonged to a plan with an open formulary. The lack of adoption can be attributed to many reasons. One reason being the advisor community has not bought into the need for formularies. Even as drug costs skyrocket, group benefit advisors fail to successfully implement the most fundamental tool for cost containment. Call to action – learn more about what formularies insurers offer and how these can help employers save. Another reason is managing change. No one likes to change. Change is work for the benefits advisor, the plan sponsor, and the employees. Strong, effective communication is a must. The report notes the perception by plan sponsors that managed formularies severely restrict access to new and existing drugs. Many of those concerns are unfounded as the majority of drugs remain available as a general benefit and only a small subset are, in fact, a non-benefit. Ultimately adopting a managed formulary ensures better management of a small subset of drugs that are costlier than existing therapies but may not offer additional value, while still maintaining open access to the vast majority of drugs on the market Still need proof? Canadian guidelines recommend metformin (cost $.20/day) as the initial agent of choice for newly diagnosed type 2 diabetes patients. Open formulary plan designs render factors like affordability irrelevant because they make all agents available at any point in the treatment journey without regard to cost-effectiveness. That is, a newly diagnosed patient could bypass metformin and/or sulfonylureas ($0.15/day) and start treatment with a costlier SGLT-2 inhibitor or a GLP-1 agonist ($2.70/day to $7.88/day) in the absence of valid clinical rationale for doing so. Emerging and future trends notes are Pharmacogenomics, Value Based Pharmacy (VBP), and Gene Therapy Pharmacogenomics: Pharmacogenomics is an exciting new field that has the potential to transform the way many common medications are prescribed. A form of personalized medicine, pharmacogenomics is based on the principle that certain genetic mutations have been shown to influence the metabolism of drugs. The goal of pharmacogenomics is to predict patient response to medications, including the potential to avoid negative side-effects. Based on pharmacogenomic information, a physician or pharmacist can initiate or modify medications that are best suited for a particular individual. The HMB+ study showed that patients whose medication treatment is optimized and guided by the results of their pharmacogenomic test can achieve better outcomes compared with patients whose treatment relies purely on clinical (i.e., pharmacist and physician) judgment. It lends support for the inclusion of pharmacogenomics in benefit plans for specific clinical scenarios to optimize patient health outcomes. That sounds great – sign me up! Not so fast. Health data is some of the most valuable and thus susceptible to cyberattacks. One must ensure that health data is sufficiently protected. Another issue is privacy. Earlier this year the Supreme Court of Canada upheld the genetic non-discrimination law which ensures Canadians can take genetic tests without being disadvantaged for insurance. But what if that changes? VBP: an important, though often overlooked determinant of success are the health care professionals themselves, specifically pharmacists. As medication therapy experts, pharmacists play an essential role in ensuring that patients’ drug therapies are safe and effective, managing patient adherence, and improving health outcomes. HBM+ implemented a VBP Program in 2018. Through the VBP Program, pharmacies in Canada (except Quebec) that submit claims to HBM+ are evaluated for the quality of care that they deliver to patients based on eight validated, evidence-based, quality-of-care measures. Gene Therapy can be considered a new paradigm in drug development that will yield hundreds of new treatments in the coming years. In fact, within the next two years, the number of approved gene therapies worldwide is expected to double. The majority of these are in the oncology space with two-thirds of active clinical trials in 2019 looking at leukemia, lymphoma, and solid tumors, but there are notable developments in treatments for cardiovascular disease, endocrine and metabolic disease, blood disorders, and ophthalmology. End.  The GAB is excited to share our first guest post. What benefits are you missing out on? From limited access due to COVID to never having used some services, our guest author Kristy Papas dives into her experience exploring with the benefits program. And not, I'm not talking about the fee coffee and tea! Although I do miss the office fruit basket.

Our body and our mind both need TLC and I am not talking about the chasing waterfalls kind. We need to take the time and opportunity to check in with ourselves. Like cars, we must have regular maintenance check ups. With this in mind, I wonder how many people realize the tools available to support this important, but often neglected, component of our lives. Putting aside the stigmas or your other priorities, there is a lot of support out there for our mental health and general wellbeing. Stop and think when did you last take the opportunity to look at what benefits your employer offers you in the way of paramedical resources or wellness spending opportunities. By paramedical, I am referring to psychologists, counsellors, registered massage therapists (RMT), physiotherapy, acupuncturists and more. By wellness spending opportunities, I mean purchasing ski passes, gym memberships, at home fitness equipment. The potential list goes on and on and on. I encourage you to stop and investigate what options are at your fingertips. Options that make important resources more affordable or accessible to you. I don’t think we should overuse our benefits as that inevitably increases premium costs for the collective whole. However, if there is a genuine need or even a general curiosity to improve your overall health and wellbeing then I encourage you to get in tune with your body and mind and identify the key areas you want to give some attention to. I know for myself two areas I really benefited from were therapy sessions for my mind and RMT sessions for my body. We spend a lot of time grinding away in a non-ergonomic work environment or perhaps not stretching before and after a workout so having someone work on any pain points or tension can be incredibly beneficial. There are also some of us that spend a lot of time internally wrestling with some important issues and struggles. Having a professionally trained, unbiased person to confide in is therapeutic. It allows us to lean into our thoughts and our feelings and hopefully gives us the capacity to outgrow them or take back the power they wield over us. No matter what you want to work on for yourself, internally or externally, I invite you to find some minutes sooner rather than later to look at what choices are available to you. Reach out to your Human Resources department or Benefits provider for more information. Your body, mind and soul, and perhaps even those around you, will be thankful for this small effort that you put in to prioritizing you. I promise you will not regret it! About our guest author: Kristy Papas is an digital content creator focusing on stop motion animation, photography, and recipe development. In a past life Kristy did your payroll! If you want you follow Kristy's work, or work with her, you can find her on Instagram, connect with Kristy on LinkedIn or through her website. 6/30/2020 What should an employee or family member expect if they reach out to the EAP provider for support?Read Now The Employee Assistance Program (EAP) is offered by employers to give employees and importantly an employee’s immediate family, access to confidential mental health support 24/7/365. Common providers in Canada are Homewood Health, Morneau Shepell (who not too long ago acquired LifeWorks and Ceridian's EAP) Aspiria, Optima Global Health, Aetna and more.

EAP’s offer short term mental health support that focuses on a specific issue. Most often you can choose to receive this support online, over the phone, or in person. EAP’s can also offer access to advisors on work and life issues including life coaching services, online resources, financial support, legal and retirement matters. What should an employee or family member expect if they reach out to the EAP provider for support? Whether you call or reach out by secure message or by text there are two things every EAP provider will do right away. First make sure that you are not in immediate danger of hurting yourself or others and second, verify your eligibility to the program with your employer information. From there, the individual at the EAP will ask questions about the reason for reaching out and determine the next steps. Depending on the needs of the caller, next steps could be speaking to someone over the phone right away or booking an appointment either over the phone or in person with someone in the caller’s area. Only mental health support is provided in person, and the program could have limitations on the number of sessions and length of session with calling for legal, financial or life coaching support. Mental Health support is fluid and adaptable to the callers needs. For example, if the caller starts with mental health support over the phone but feels their needs would be better served in person, that can be arranged. Mental health support and support for one’s work and life issues require effort on the users end. Just like with a visit to the physiotherapist, callers may be given “homework” such as cognitive behavioural therapy exercises, or they may need to practice using the tools provided to them. Employees and their families should know that these services are confidential. Their employer will not know that the service was used. I encourage everyone who has access to an EAP to at a minimum check out your provider’s online tools via the app or website. It is an excellent source of information and resources. Remember, no issue is to small. The hardest step for most of us is the first step, asking for help. But help is available. WeThere is nothing usual about anything right now. How, where, and if people are even working has dramatically changed. Employee benefit plans have not been immune to the changes brought on by COVID-19. One positive change to benefit programs is that many insurers have fast tracked the employee digital experience, especially when it comes to disability claim submission.

From a cost perspective, what should employers expect as social distancing is relaxed and employees return to the workforce? This is a complex question with a lot of moving parts; in the short-term costs will likely increase. Let’s break it down across each line of benefit to examine how the cost of the benefit will increase. The “pooled” benefits: Life insurance, disability, and critical illness insurance The rates for these benefits are set using the demographic mix of the plan and they are renewed with little to no individual claim usage. The premium for these benefits will increase for a few reasons, the first reason is low interest rates. Interest rates play an important role in both the rate setting and renewing of these benefits because insurers invest these premiums. As interested rates drop, the premium for these benefits will eventually increase. We saw this after the 2008 recession and insurers were already making rate adjustments pre-COVID-19. Since the Bank of Canada reduced the key interest rate to a record low of 0.25 in March 2020, you can expect higher than average increases to all these benefits. The second reason you can expect rates to increase for disability insurance is an increase in claims combined with more LTD back to work programs. Mental health claims already had the #1 spot for the cause of disability. Isolation, financial worries, increased anxiety, and a general higher level of stress will likely lead to an increase in short and long-term disability claims. A recent article in the Benefits Canada magazine stated that half of Canadians reported a worsening of their mental health with 10 per cent saying it has worsened a lot. Mental health claims may not be the only claim cause on the rise. Working from home could bring an increase in musculoskeletal claims. Poorly set up workstations can be the cause of several different types of injury. When you combine this with an overall decrease in daily movement and activity, employees are at a greater risk of injury. HealthLink BC explores the topic of workplace ergonomics. Healthcare: Vision, paramedical practitioners, hospital (semi/private room), medical supplies Overall, these benefits will have a temporary decrease in claims followed by a temporary spike in claims once practitioners reopen. There is an exception to this: vision care. Vision claims will be minimally affected if at all. Most vision care benefits have a rolling 12-24-month claim period. Couple that with the ease of ordering glasses and contacts online means the claim activity on this benefit should be similar to pre-COVID-19 levels. Claim activity for most paramedical practitioners will fall to zero since they are not accessible. There are digital options available for physiotherapy and psychology which will see some claim activity. Once these businesses reopen, there will be a large, temporary spike in claims. With elective surgeries postponed, hospital room claims have also dropped significantly. Like the paramedical benefit once elective surgery resumes, there will be a claim spike. Medical supplies usually make up a small percentage of the total healthcare claims and don’t have a major impact on the rates an employer pays. This benefit line will also have a temporary lull in claims as most suppliers are closed. Many supplies have a multi-year benefit maximum which may have already been reached or require referrals from specialists or physicians. Supplies like orthotics that are a nice to have for most people will not be a priority. Prescription Drugs We covered how COVID-19 is temporarily increasing the costs of your prescriptions in this article. Post-COVID-19 should see drug claims eventually return to pre-COVID-19 levels with an exception. Inactivity, stress, and other lifestyle factors can lead to preventable chronic conditions such as heart disease and type 2 diabetes. It’s possible that there will be an increase in these conditions, which would lead to a long-term increase in claims unless reversed with lifestyle. Dental Dental Claims came to a screeching halt as dental offices were forced to close. With the exception for emergency dental (which often falls into healthcare anyway) claims are at zero. Just like most of healthcare, pent up demand will cause a huge spike in claims when offices re-open. Dental is a unique benefit. It’s important to consider the dental recall schedule, rolling frequency for items such as scaling and plan maximums that could be calendar year or benefit year. Some plan members may have maxed out their dental coverage before offices closed, while others are overdue for work. Many pre-COVID-19 dental claim analysis will reveal a scenario where claims were already above the budgeted amount. Other considerations: Premium Relief, employees returning to work and layoffs All the Insurers have given temporary premium relief in the form of a credit to non-refund plans. Most offered employers a 10% credit on the total healthcare premium and 50% for the dental premium. Credits are being reflected in May and June billing statements and are being assessed regularly by the insurers. The purpose of this credit is to support businesses during this time of crisis and to reflect the fact that many of these services are unavailable. Employees who were laid off with benefits will have the same impact on claims as those employed and on the benefit program. Post COVID-19 new hires will likely also have pent up demand for claims. The fight for talent is going to change and employers may need to offer incentives like waiving the waiting period to join the plan. What does all this mean for employers and the cost of employee benefit programs? Employers should try to budget for a higher than average increase in premiums across all benefits. The lower claims on health and dental that would have means rate decreases are being negated by the premium relief and the inevitable spike in claims. New normal. Post-COVID. The re-opening. Whatever you want to call it, how people work and how we do business is changing. During the early days of the COVID-19 crisis when employers were looking for ways to cut the cost of doing business, they discovered the rigidity of their employee benefit program. Scaling back benefits is limited to underwriting rules (which insurers bent or revised) and software limitations. Many small business benefit plans are cookie cutter plans built in a technology platform created in the 90’s. Want proof? Sun Life’s Designed for Health papers show how most benefits programs remain unchanged for decades and that most employers are offering the same level of coverage.

Employee survey after survey show that there is a want for plan choice. And the need from employers for plan flexibility will push insurers to update their technology and change not only how benefits are delivered but what options are available to employers and employees. What could a plan redesigned for flexibility look like? Employee benefits programs were originally designed to offer insurance to employees. Life, disability, and expensive healthcare items. Over time, low cost items and day to day expenses like massage, vision care and dental were added to plans. Would you pay $550 every year to insure a $500 bicycle? No, you wouldn’t, but that’s exactly what employers are doing with benefits like massage. This traditional plan design of one size fits all, doesn’t fit anyone. And the traditional concept of insuring day to day health and dental expenses doesn’t make good business sense. The future of benefits is personalized coverage and portability. Flex plans, which offer some personal choice, are already a popular choice for larger employers. Equitable Life has successfully delivered a great scaled down version of this plan design for small businesses. Imagine an employee having the flexibility to claim day to day expenses that they determine are important, combined with insurance protection. Imagine how that personalization will engage employees and provide them value. This plan option also gives employers a set, predetermined budget for a large portion of benefit program spend plus the flexibility to adjust their spend in steep economic downturns and future unexpected events such as a pandemic. Smart use of AI is already happening with promopts in carriers apps and plan members portals. That's the personalization. The portability piece is a challenge that I'll review in another post. With pharmacies moving prescriptions from a 90-day to a 30-day supply there are many considerations for plan sponsors. Benefits Canada outlines some of these in their latest article. In it, Suzanne Lepage reminds us that “It’s worth making sure that plan members are not penalized because of a new mandate that’s out of their control.” While plan sponsors are currently benefiting from premium relief on low utilization benefits such as vision and dental, they should be preparing for higher than usual drug claims.

Drug costs will increase as a result of the 30-day supply, how much will vary from group plan to group plan. Let’s say you have 3 monthly scripts, the pharmacy charges about $10/script in disp fees every three months, or $30. Now, that cost has tripled to $90/3 months. The 30-day supply could also have a negative affect on plan member adherence to their prescriptions, which we know has a negative affect on claims and overall health outcomes. The 30-day supply isn’t the only way that drug usage is increasing. This early US-based data found that prescriptions for mental health conditions such as anxiety have increased by 21% since COVID-19. Other plan features that we should keep an eye on are PPNs and drug formulary flexibility if/when a drug shortage happens. Prescription drugs are usually the most claimed item in a benefit plan. When addressing ways to reduce the claim cost for drugs, it’s important to remember why the drug coverage is being offered. A group benefits plan has three purposes. First it protects employees from a catastrophic loss due to health. This is insurance. Today, even common chronic conditions like high cholesterol can cost almost $10,000 per year; this firmly places drug coverage in the insurance category. Second, it acts as compensation with coverage for day to day expenses like dental, vision and health services like massage. Third, the plan supports employee’s health in a preventative manner.

Keeping in mind that drug coverage is insurance, I have categorized solutions into four buckets. Bucket #1: Plan Design There are two basic plan design features that should be part of every plan:

Other plan options:

It may be tempting to put a maximum on drugs. Avoid this if possible. Even a maximum of $50,000 limits the drug insurance and your employee’s ability to access a life saving drug. Drug maximums also pose an ethical dilemma and could be seen as a fundamental change to compensation especially when you have an employee or dependent using a high cost drug. Formularies such as those offered by the Reformulary Group are under utilized ways for employers to keep their drug plan sustainable while encouraging employees to make informed, smart drug choices. Bucket # 2: Increased adherence to medications Adherence to prescriptions reduces the overall cost of a plan member’s chronic condition, especially those with multiple chronic conditions. One way to increase adherence is with a dispending fee frequency limit (DFFL). This is not to be confused with a dispensing fee cap. The DFFL sets a threshold for the number of dispensing fees paid for by your plan for maintenance drugs only. A DFFL encourages plan members to fill maintenance drugs in three-month supplies which is known to increase adherence to medication There are other programs that can help increase adherence such as the online pharmacy PocketPills. PocketPills combines personalized packing with technology to manage an employee’s medications. Their system helps employees remember to take their medications as prescribed by their physician, plus they have a low mark up and dispensing fee. Bucket #3: Preventative healthcare Preventing drug claims from happening in the first place is the best way to keep drug cots low. Many chronic conditions can be prevented with lifestyle and fostering a culture of wellness. Focusing on mental, physical and financial health will positively impact your claims. Many insurers have free wellness programs and mental health support built into your plan for free. Bucket #4: Education Do you and your employees know about the programs available to you from your insurer? What programs does your local pharmacist offer? What about online and mail order pharmacies? What do employees know about shopping for the best price for prescriptions? Do employees know how to manage their conditions? Are employees using the technology provided by the insurer? Insurers have built in a lot of resources, programs, and tools for employees. But employees can’t utilize these if they don’t know they are there. Ask your advisor what your insurer offers and have an employee communication strategy. Firstly, it’s important to cover why protecting employees’ mental health is so important. Why should employers care enough to protect their employee’s mental health? After all, the workforce is changing and employee loyalty is waning. Ultimately it’s the right thing to do, but there is also a strong business case to be made for protecting employee mental health.

According to the Canadian Mental Health Association (CMHA) half of Canadians will have suffered from a mental illness by age 40. Mental illness is also a leading cause of disability in Canada, accounting for 30% of claims and 70% of all disability costs. Given that the cost of disability leave for mental illness is about double the cost of a leave due to physical illness, that’s a significant impact to employers. Mental illness is also often an underlying secondary cause of disability when physical illness or accident is the primary cause. And that’s just the financial tip of the iceberg. Laying underneath is the cost of presenteeism and absenteeism that poor mental health can have on a business. So – back to the original question: what can employers do? There is a lot to consider when it comes to mental health and many employers may not know how or where to start. Here’s what I recommend to begin: Employers can start by reviewing the Centre for Addiction and Mental Health (CAMH)’s Mental Health Playbook for Business Leaders. The playbook outlines five research-informed recommendations for employers to begin bringing mental health to the forefront. I also recommend reading about the National Standard for Psychological Health and Safety in the Workplace– “the first of its kind in the world, is a set of voluntary guidelines, tools, and resources intended to guide organizations in promoting mental health and preventing psychological harm at work”. Employers can also access resources from Not Myself Today, including an informational kit to help them get started! Include Mental Health in Employee Benefits It’s common practice for employers to incorporate support for mental health in their total compensation strategy, namely in the benefit plan. The Employee and Family Assistance Program (EAP) is something that many employers may already be familiar with. The EAP supports employees to resolve work, health and life issues. The EAP is an effective, but underutilized product. A newer tool in the benefits box is iCBT or internet-based Cognitive Behavioral Therapy. iCBT is digital therapy guided by a registered mental health professional. iCBT can be claimed through the psychologist benefit in most benefit plans. Other ways that employers can support employee mental health through their total compensation package, is to include generous time for personal days. Notice that I didn’t say sick days. Stigma around mental health is still an issue and the language we use to break down stigma matters. Allocating personal days to employees gives them the flexibility to take a day off, whether it be for a physical or mental illness. Removing barriers to access care and time off, such as a doctor’s note, is an easy change that employers can implement right away. Build Support from Top-Down Beyond the basic support available to employees in their benefits, building support for employee’s mental health must come from the top down. Leadership must be invested in supporting employee’s mental health and they must practice what they preach. Otherwise programs fall flat, and employees won’t buy what leadership is selling. Ultimately the support needs to be part of the company culture. Employers should be careful not to confuse supporting employee wellness with employee mental health and mental illness. Workplace wellness initiatives usually support healthy behavior in the workplace with the goal of improving health outcomes. These programs may include activity challenges, flu clinics, gym memberships, lunchtime yoga or mindfulness and more. Wellness initiatives can support mental health, but it is in a separate category from mental health initiatives. When it comes down to it, little budget, big-budget, or no budget there’s something every employer can do to support employees and their mental health. This article was originally posted on February 25, 20202 in the Benefits by Design Ask the Advisor segment. |